Weekly Review: March 17 - 21, 2026 | The Fed Holds, Oil Surges, and Markets Test Your Patience

What Happened, What It Means, and What You Might Do About It

This was one of those weeks where the headlines felt louder than the actual damage. Markets swung hard on war developments, oil prices, a Fed meeting, and enough uncertainty to make even seasoned investors question whether they should be doing something. The short answer: probably not. But let's break down what actually happened.

The Big Picture

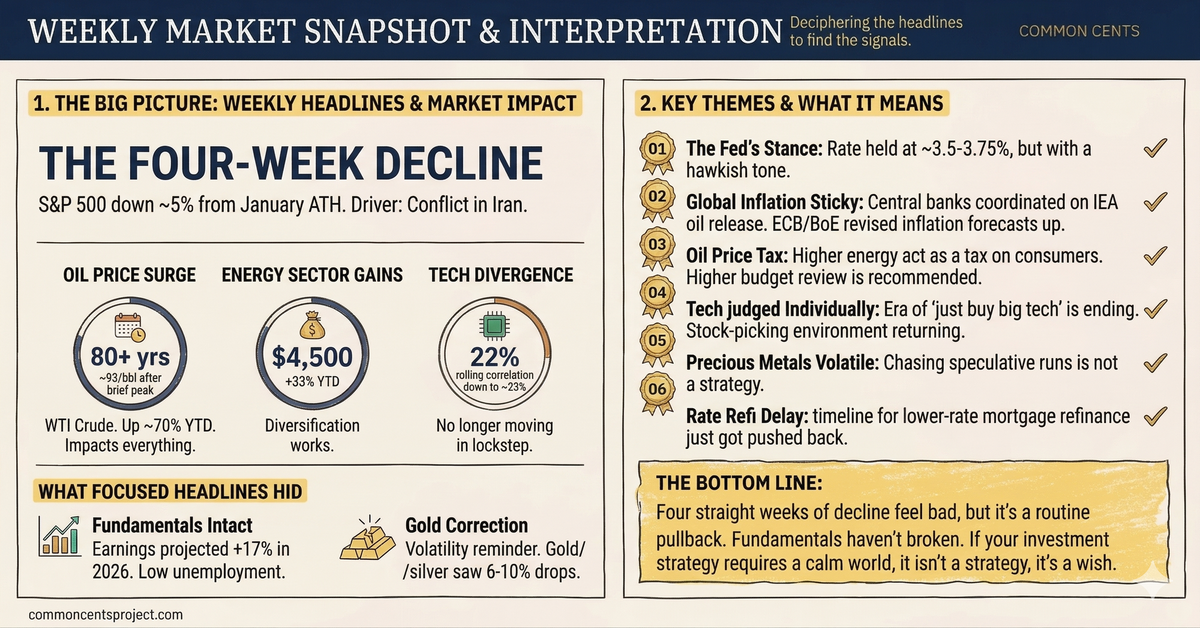

The S&P 500 fell for a fourth straight week, now sitting about 5% below its January all-time high. The Dow closed below its 200-day moving average for the first time this year. The Nasdaq slid further into correction territory on weakness in mega-cap tech names. It wasn't a bloodbath, but it wasn't comfortable either.

The driver of all of it? The ongoing conflict in Iran. Oil prices have surged roughly 70% since the start of the year, with WTI crude hovering around $93 per barrel after briefly touching $100. That's not just a number on a screen. That's your gas bill, your grocery bill, and the cost of shipping everything you buy. When oil moves like this, it ripples through the entire economy.

The Fed Held Rates Steady (But That's Not the Whole Story)

On Wednesday, the Federal Reserve voted 11-1 to keep interest rates at 3.5% to 3.75%. No surprise there. What mattered more was the tone.

Fed Chair Jerome Powell acknowledged that inflation isn't coming down as fast as they'd hoped. The Fed raised its 2026 inflation forecast to 2.7%, up from 2.5% in December, citing tariffs and the energy shock from the Middle East. The dot plot still projects one rate cut this year, but markets aren't buying it. Traders are now pricing in roughly a 75% chance of no cuts at all in 2026, and some are even pricing in the possibility of a hike.

Powell summed up the uncertainty with a line that tells you everything: "If we were ever going to skip a Summary of Economic Projections, this would be a good one."

What this means for you: If you're carrying variable-rate debt (credit cards, adjustable-rate mortgages, HELOCs), rates aren't going down anytime soon. If you were counting on lower mortgage rates to refinance, that timeline just got pushed back. On the flip side, money market funds and high-yield savings accounts are still paying well north of 4%, so your cash is earning decent returns while we wait for clarity.

Oil, Energy, and the Inflation Question

The International Energy Agency coordinated the release of 400 million barrels of crude oil, the largest such action in the agency's history. Saudi Arabia also ramped up production. Despite all of that, prices remain elevated because the market is pricing in a prolonged disruption.

Energy stocks are up 33% year-to-date, making the sector the clear winner in 2026 so far. Financials, on the other hand, are down 11% as the yield curve has flattened aggressively, squeezing bank margins.

What this means for you: Higher energy costs act like a tax on consumers. Every dollar you spend on gas is a dollar you're not spending (or saving) somewhere else. If you haven't revisited your budget since oil was $60, now would be a good time. Also, if you're a long-term index fund investor, know that your S&P 500 fund is doing exactly what it's supposed to do: the energy stocks in it are offsetting weakness in other sectors. That's diversification working in real time.

Tech and AI: Still Alive, but Bumpy

NVIDIA had a strong week despite the broader selloff, boosted by CEO Jensen Huang's announcement at the company's developer conference that expected purchase orders for its chip platforms could reach $1 trillion by 2027. That's a staggering number.

But the rest of big tech didn't fare as well. Amazon, Apple, and Microsoft all declined, and the software sector is down roughly 20% from its highs. The "Magnificent Seven" are no longer moving in lockstep. Their rolling 3-month correlation has dropped to 23%, down from an average of 56% over the prior two years. Translation: these stocks are being judged on their individual merits now rather than riding a wave together.

What this means for you: If you own a broad market index fund, this is actually healthy. Dispersion (stocks moving independently of each other) is what protects diversified portfolios from sharp, uniform declines. It also means the era of "just buy big tech" may be giving way to a more traditional stock-picking environment. For most of us, that changes nothing about strategy. Keep investing in your index funds.

Gold and Silver Got Crushed

Here's one that caught a lot of people off guard. Gold dropped over 6% to around $4,285, and silver fell nearly 10%. Both precious metals are now in the red for the year after a massive speculative run-up driven partly by retail traders.

What this means for you: If you bought gold as a "safe haven" in the last few months, this is a reminder that safe havens can be volatile too. Gold tends to do well during uncertainty, but when that uncertainty is accompanied by rising real interest rates (which make bonds more attractive), gold can sell off even in scary times. The lesson: gold can have a place in a diversified portfolio, but chasing it after a big run-up is speculation, not strategy.

The Dollar Strengthened

The U.S. dollar rose about 2% in March against a basket of currencies, playing its traditional safe-haven role. A stronger dollar makes imports cheaper (helping consumers) but hurts U.S. companies that earn revenue overseas (hurting earnings for multinationals).

Global Central Banks Are All in the Same Boat

It wasn't just the Fed. The Bank of England, European Central Bank, and Bank of Canada all struck cautious tones last week. The ECB raised its 2026 inflation forecast to 2.6% and cut its growth outlook. The Bank of England held rates and removed language about future cuts. Bond markets are now pricing in the possibility that some central banks may need to hike rates if the energy shock persists.

What this means for you: This is a global problem, not a U.S.-specific one. If you hold international funds, expect similar headwinds. The silver lining is that central banks are coordinating (the IEA oil release is a good example), which historically helps stabilize markets faster than unilateral action.

The Bottom Line for This Week

Four straight weeks of declines feels bad. A war, rising oil, sticky inflation, and a Fed that can't cut rates feels worse. But context matters.

The S&P 500 is down about 5% from its all-time high. That's a routine pullback. The market experiences an average of three 5% pullbacks and one 10% pullback every calendar year. We're right on schedule. S&P 500 earnings are still projected to grow 17% in 2026. The economy is expanding at a solid pace. Unemployment is low. The fundamentals haven't broken.

Weeks like this are the price of admission for long-term returns. If your investment strategy requires a calm, predictable world to work, it isn't a strategy. It's a wish.

Keep contributing. Stay diversified. Don't make permanent decisions based on temporary headlines. The boring stuff still works.