Opportunity Cost: The Hidden Price of Right Now

The Bottom Line: Every dollar you spend has two costs: the price tag, and what that dollar could have become. Opportunity cost is the reason some people build wealth and others wonder where it all went. Understanding it doesn't mean you stop enjoying life. It means you start enjoying it on purpose.

Every financial decision you make has a visible cost and an invisible one. The visible cost is the number on the receipt. The invisible one is what that money could have become if you'd done something else with it.

That invisible cost has a name. Economists call it opportunity cost. And it might be the most important concept in personal finance that almost nobody thinks about.

The $7 That Becomes $70

When you spend $7 on a coffee, you're not just spending $7. If you invested it instead and earned an average market return of around 10% per year, that $7 becomes roughly $70 in 25 years. You didn't lose $7. You lost $70.

Now scale that up. A $50,000 car instead of a $30,000 one. A $2,000 weekend trip on a credit card you won't pay off for months. Each decision carries a visible price and an invisible one. The invisible one is almost always bigger.

This isn't an argument against spending money. It's an argument for knowing what your spending actually costs.

Your Brain Is Working Against You

Humans are hardwired for immediate gratification. For most of human history, if you found food, you ate it. The future was uncertain and short, so optimizing for right now made sense.

The problem is that we're running ancient software in a modern world. You will, statistically, live into your seventies or eighties. You will need money when you can no longer work or when you no longer want to. But your brain doesn't feel the future. It feels right now. The new phone is real and tangible. The retirement account is abstract and decades away.

And every app, ad, and algorithm in your life is designed to reinforce that impulse. One-click checkout. Same-day delivery. Buy now, pay later. The modern economy is engineered to make spending frictionless and saving feel like punishment.

You're not weak for feeling the pull. You're human. But understanding the game is the first step toward not losing it.

The Marshmallow Problem

In the 1960s, Stanford researchers put a marshmallow in front of a child and gave them a choice: eat it now, or wait fifteen minutes and get two. The kids who waited went on to have better outcomes by almost every measurable standard — test scores, health, financial stability.

Your finances work the same way. Every spending decision is a marshmallow test. The good news is that unlike a four-year-old, you can build systems that make waiting the default. More on that in a moment.

Small Decisions, Massive Consequences

It's rarely one big purchase that derails your finances. It's hundreds of small ones, each individually harmless, that collectively add up to tens of thousands of dollars a year that never get invested and never compound.

Consider two people, both earning $75,000. One spends an extra $500 a month on impulse purchases and lifestyle upgrades that feel necessary but aren't. The other invests that same $500 into an index fund. After 20 years, the second person has roughly $345,000. The first has memories of meals they can't quite remember and things they no longer use.

That's a $345,000 decision made $500 at a time.

The person who starts investing $300 a month at 25 will have over a million dollars by 60 at average market returns. Wait until 35 to start the same habit and you'll have less than half that. The cost of those ten years isn't $36,000 in missed contributions. It's over $500,000 in missed growth.

Spend More on What Matters. Cut the Rest.

Let me be clear: this is not a lecture about living on rice and beans. Life is meant to be enjoyed, and your money should be part of how you enjoy it. Take the trip. Go to the nice dinner. Buy the thing that genuinely makes your life better. You should absolutely reward yourself, and you should do it without guilt.

The distinction is between spending that's intentional and spending that's unconscious. The $200 dinner with friends you've been looking forward to all month? That's money well spent. The $15 DoorDash order on a random Tuesday because you're bored? That's not a reward. That's a habit. And habits like that are the silent killer of long-term wealth.

Spend extravagantly on what you love. Cut ruthlessly on what you don't. The goal isn't to spend less. It's to spend right. The person who spends $5,000 a year on travel they'll remember forever is in a better position than the person who spends $5,000 a year on subscriptions they forgot they had.

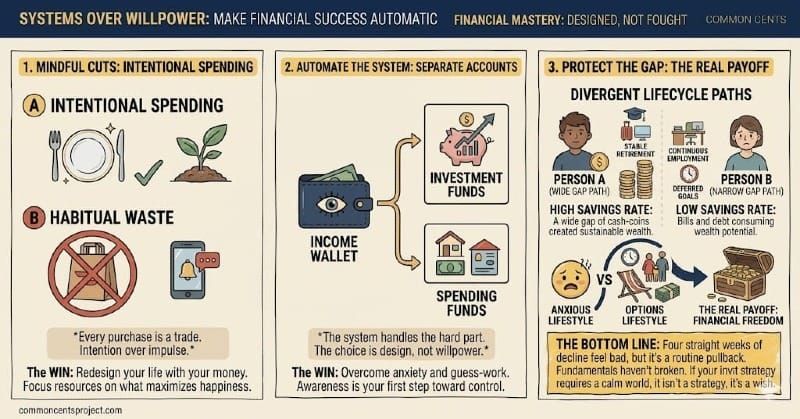

Build the System, Not the Willpower

Willpower is a terrible long-term strategy. The key is making the right choice the easy choice. Automate your savings so the money moves before you see it. Set your 401(k) to increase by 1% each year. Use separate accounts so your spending money and your investment money never share a roof.

When the system handles the hard part, you don't have to fight your brain every day. You save automatically, invest consistently, and then spend what's left, freely and without anxiety, because you know the important stuff is already taken care of.

That's the real payoff. Not deprivation. Not restriction. The freedom to enjoy your money today because you've already taken care of tomorrow.

Every purchase is a trade. Make sure you know what you're trading for.

Want to see what your habits are actually costing you? Check out our Opportunity Cost Calculator to plug in your own numbers and find out what your spending could become if you put it to work.