Weekly Market Review: March 30 – April 3, 2026 | Stocks snapped a five-week losing streak, but $128 oil and no ceasefire kept the celebration short.

Week at a Glance

| Benchmark | Close (April 2) | Weekly Change |

|---|---|---|

| S&P 500 | 6,582.69 | +3.4% |

| Dow Jones | 46,504.67 | +3.0% |

| Nasdaq | 21,879.18 | +4.4% |

Markets were closed Friday, April 3 for Good Friday. Oil prices dominated the week, with the U.S. Energy Information Administration reporting that Brent crude reached nearly $128 per barrel intraday on Thursday. The national average price of regular gasoline crossed $4.00 per gallon for the first time since August 2022, according to AAA.

Markets: The First Green Week Since February

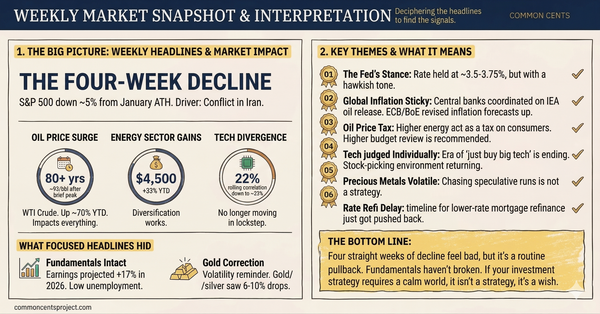

The S&P 500 snapped a five-week losing streak, rising 3.4% and closing Thursday at 6,582.69. It was the index's first positive week since the week ended February 20. The Nasdaq climbed 4.4% and the Dow gained nearly 3% after both had entered correction territory the prior week.

Tuesday was the catalyst. An unconfirmed report that Iranian President Masoud Pezeshkian was open to ending the war sent stocks surging. The Dow gained 1,125 points (2.49%) to close at 46,341.51, the S&P climbed 2.91% to 6,528.52, and the Nasdaq rallied 3.83% to 21,590.63. It was the best single day for all three indexes since May.

The momentum faded by Thursday. Brent crude spiked toward $128 per barrel intraday, and President Trump's prime-time address Wednesday evening promised more military action rather than a ceasefire. Markets gave back some of Tuesday's gains as the reality set in that the conflict is far from over. The Dow finished Thursday down 61 points while the S&P and Nasdaq eked out fractional gains.

March 31 also closed out the first quarter. The S&P 500 fell 5.1% in March and 4.6% for Q1, its first quarterly decline in a year. The quarter started with optimism and ended with a war.

What This Means for You: One good week does not mean the volatility is over. But it does mean the five-week freefall has paused. If you stayed invested through all five of those down weeks, you just participated in a 3.4% recovery. That is exactly how long-term investing works. The people who sold during the losing streak missed it.

Oil: Approaching $130 and What It Costs You

Brent crude reached nearly $128 per barrel intraday on Thursday, according to the U.S. Energy Information Administration. The Brent-WTI spread widened to $25 per barrel on March 31, the largest gap in over five years, reflecting the direct impact of the Strait of Hormuz closure on international oil flows.

The numbers tell the story of how fast this escalated. Brent started the year at $61. It finished the quarter at $118. The EIA called the Q1 price increase the largest on an inflation-adjusted basis in data going back to 1988. Roughly 20% of the world's oil supply normally moves through the Strait of Hormuz, and that traffic has been reduced to a trickle since late February.

At the consumer level, the national average price for regular gasoline crossed $4.018 per gallon, according to AAA. Gas prices have risen more than 30% since the conflict started.

What This Means for You: Oil above $100 is not just a number on a trading screen. It shows up in your gas tank, your grocery bill, your heating costs, and your airline tickets. If you have not revisited your monthly budget since February, now is the time. Look specifically at transportation and food, because those categories are absorbing the biggest price increases. If you have summer travel planned, lock in what you can now. Prices are unlikely to come down quickly even if a ceasefire holds.

Trump's Prime-Time Address: Escalation, Not Resolution

On Wednesday evening, President Trump addressed the nation from the White House on the Iran war, now in its second month. The speech did not deliver the ceasefire many investors hoped for. Instead, Trump said U.S. military objectives were "nearing completion" and promised to hit Iran "extremely hard over the next two to three weeks." He also referenced discussions with "more reasonable" Iranian leaders, though Tehran immediately denied any active negotiations.

The speech came one day after the huge Tuesday rally, driven by hopes for exactly the kind of diplomatic breakthrough that did not materialize. Iran's position remains unchanged: no ceasefire without conditions, and no reopening of the Strait of Hormuz while under attack.

What This Means for You: Markets rallied on hope and gave back gains on reality. This pattern will repeat as long as the conflict continues. Headlines about imminent deals and talks breaking down will whipsaw stocks and oil in both directions. Your response should be the same either way: do not make portfolio changes based on a headline. Let your automation run. Check your budget, not your brokerage account.

The Economy: Mixed Signals, One Bright Spot

Several important data releases landed this week.

Consumer Confidence edged up to 91.8 in March from 91.0 in February, according to the Conference Board. The headline improved, but households reported higher inflation expectations, shifted big-ticket purchase plans from "yes" to "no," and expressed growing anxiety about the labor market. Foreign travel plans collapsed, likely due to the conflict abroad.

The JOLTS report showed job openings fell to 6.882 million in February, down 358,000 from the prior month. Hiring dropped to 4.849 million, the lowest level since March 2020 and, outside the pandemic, the lowest since August 2014. Accommodation and food services, healthcare, and construction saw the steepest declines.

ISM Manufacturing PMI rose to 52.7 in March, the highest reading since August 2022 and the third straight month of expansion. Production accelerated. But the prices subindex surged to 78.3, the highest since June 2022. About 40% of negative manufacturer comments cited the Iran war, while 20% cited tariffs. Factories are busy, but their costs are climbing fast.

Retail Sales for February came in at +0.6% month over month, beating expectations. Clothing, auto sales, and e-commerce were strong. But the data does not yet reflect the full impact of rising fuel costs, which began hitting consumers hardest in March.

The big number came on Good Friday. The March jobs report showed 178,000 jobs added, the most since December 2024 and well above the Dow Jones consensus of 59,000. The unemployment rate ticked down to 4.3% from 4.4% in February. Healthcare drove much of the rebound as Kaiser Permanente strike workers returned, adding 76,000 jobs. Average hourly earnings rose 0.2% to $37.38. February's payrolls were revised sharply lower, from -92,000 to -133,000.

What This Means for You: The jobs report was the best news of the week, and the market could not even trade on it. The labor market is still adding jobs, unemployment is holding steady, and wages are growing moderately. That combination supports the economy without adding fuel to inflation. As long as people are employed and earning, the foundation holds. But the JOLTS data is a warning sign: hiring is slowing. If you are job hunting, do not wait. The environment is getting more competitive.

What to Watch Next Week

Monday will be the first time markets can react to the strong jobs report. Expect movement at the open, but oil prices will determine how much of any rally holds.

The critical deadline is April 6, when Trump's timeline for Iran to reopen the Strait of Hormuz expires. Any progress, or escalation, will move oil and equities in opposite directions.

On the data calendar, the March CPI (consumer price index) release will be important. With energy prices surging, headline inflation is expected to jump. The question is whether core inflation, which strips out food and energy, remains contained. If it does, the Fed can stay patient. If it does not, rate hike talk comes back into the conversation.

First quarter earnings season also kicks off next week. Bank earnings from Goldman Sachs, JPMorgan, and others will give the first real look at how corporate America is handling the new environment.

The Bottom Line

This was the week the market exhaled. After five straight weeks of losses, stocks posted their first gain of the spring. The rally was real, but so is the context: it was driven by ceasefire hopes that have not materialized, and it occurred against a backdrop of oil approaching $130, $4 gasoline, and a president promising more military action.

The good news is that the economy is still functioning. Jobs are being created. Factories are expanding. Consumers are spending. That foundation matters more than any single week of stock performance.

Your job this week is the same as it was last week and the week before that: keep contributing to your retirement accounts, keep your emergency fund accessible, revisit your budget if gas and grocery costs have changed your spending, and resist the urge to trade on headlines. The March jobs report is a reminder that the economy is more resilient than the news cycle suggests. Stay the course.