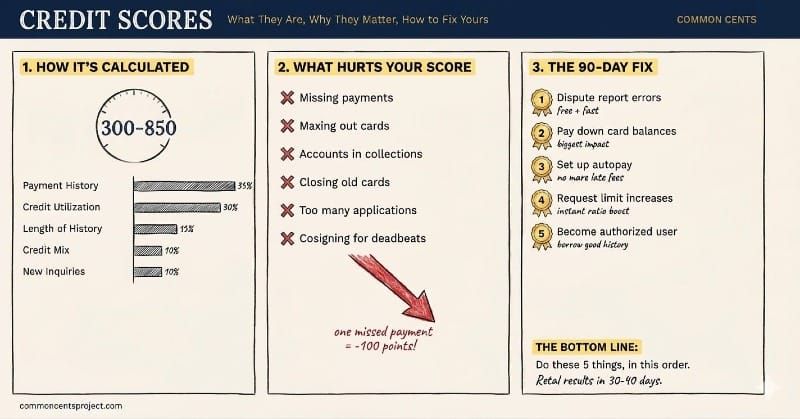

Credit Scores: What They Are, Why They Matter, and How to Improve Yours.

The Bottom Line: Your credit score is a three-digit number (300 to 850) that determines what you pay for mortgages, car loans, insurance, and more. The same house can cost you tens of thousands more with a low score than a high one. The good news: the rules are simple, the game is winnable, and most people can see real improvement in 30 to 90 days.What it is: A FICO score based on five factors: payment history, credit utilization, length of history, credit mix, and new inquiriesWhat kills it fastest: Missed payments, maxed-out cards, accounts in collections, and closing old cardsWhat builds it fastest: On-time payments, keeping balances below 10% of your limit, and disputing errors on your credit reportThe fastest fix: Pull your credit reports, dispute errors, pay down card balances, set up autopay, in that order

Your credit score is your financial GPA. It's a three-digit number, ranging from 300 to 850, that tells lenders, landlords, insurers, and even some employers how well you've managed borrowed money. You didn't choose to play this game, but you're in it. And the rules are worth knowing.

The most widely used score is the FICO score. Above 740 is excellent. Between 670 and 739 is good. Between 580 and 669 is fair. Below 580 is poor. That single number has an outsized impact on your financial life, and the difference between a good score and a great one can cost (or save) you tens of thousands of dollars.

Consider a mortgage. The same house, the same income, the same down payment, but the person with a 760 credit score might pay significantly less in interest over the life of the loan than the person with a 660. That's not a different house. It's the same house with a different price tag, determined entirely by three digits.

How Is Your Credit Score Calculated?

Five factors, in order of weight:

Payment history (~35%): Have you paid your bills on time? Even one missed payment can leave a mark that lasts years. This is the single biggest factor, and it's the one entirely within your control.

Credit utilization (~30%): How much of your available credit are you using? If you have a $10,000 limit and carry a $9,000 balance, that 90% utilization rate is dragging your score down hard. Keep it below 30%, and ideally below 10%.

Length of credit history (~15%): Older accounts help. The longer your track record of responsible borrowing, the more confidence lenders have in you.

Credit mix (~10%): A variety of credit types (cards, auto loans, a mortgage) shows you can manage different kinds of debt responsibly.

New credit inquiries (~10%): Every time you apply for credit, a "hard inquiry" hits your report. A couple is fine. A dozen in a month signals risk.

What Hurts Your Score the Most

Not all mistakes are created equal. These are the habits and actions that will do the most damage to your credit score, some of them faster than you'd expect.

Missing payments. This is the single most destructive thing you can do. One payment that's 30 or more days late can drop your score by 50 to 100 points, and that mark stays on your credit report for seven years. The more recent the missed payment, the harder it hits. Two or three missed payments in a row and you're in serious trouble.

Maxing out your credit cards. Carrying balances close to your credit limit signals to lenders that you're overextended. A utilization rate above 50% is actively damaging your score every single month it's reported. Even if you pay the balance off eventually, the damage compounds while it sits there.

Defaulting on debt or going to collections. When a creditor gives up on collecting from you and sells the debt to a collections agency, it's one of the worst marks your credit report can carry. It tells future lenders that you didn't just pay late. You didn't pay at all.

Closing old credit cards. This is one of the most common well-intentioned mistakes people make. Closing an old card shortens your credit history and reduces your total available credit, which raises your utilization ratio. That card you opened ten years ago with a zero balance? It's quietly helping your score just by existing. Leave it open.

Applying for too much credit at once. Every application triggers a hard inquiry. One or two won't matter much, but a flurry of applications in a short window looks desperate to lenders and can knock your score down several points per inquiry.

Cosigning for someone who doesn't pay. Their missed payments become your missed payments. Their default becomes your default. Cosigning is a generous act that can destroy your credit if the other person doesn't hold up their end.

What Helps Your Score the Most

The good news is that building and maintaining a strong credit score isn't complicated. It's not exciting either, but the habits that matter are simple and repeatable.

Pay every bill on time, every time. This is the foundation. Set up autopay for at least the minimum payment on every account you have. There is no excuse for a late payment in the age of automatic billing. If you do nothing else on this list, do this.

Keep your credit utilization low. Pay your credit card balances down, or ideally off, every month. If you can't pay in full, at least get the balance below 30% of your limit before your statement closing date, because that's the number that gets reported to the credit bureaus. One trick: if you make a large purchase, pay it off before the statement closes so the high balance never gets reported.

Don't close old accounts. That credit card you opened in college but never use anymore? Keep it open. It's adding years of history to your report and increasing your total available credit, which keeps your utilization ratio low. Just make sure there's no annual fee eating into you.

Check your credit report at least once a year. Go to AnnualCreditReport.com, the only free, government-authorized source, and pull your report from all three bureaus: Equifax, Experian, and TransUnion. Look for errors, fraudulent accounts, and incorrect balances. Disputes can be filed online, and about one in four Americans have errors on their reports. A single mistake could be costing you real money right now, and fixing it is free.

Request credit limit increases. If you've been a responsible cardholder for a year or more, call your card issuer and ask for a higher limit. If your limit goes from $5,000 to $10,000 and your balance stays at $1,500, your utilization just dropped from 30% to 15%. That's an instant boost without spending or paying a dime. Just don't use the new credit as an excuse to spend more.

Let time work for you. A longer credit history helps your score. Every month that passes with on-time payments and low utilization is a month that strengthens your profile. This is the unsexy truth about credit: the single best thing you can do is start building good habits and then be patient.

If You Want to Improve Your Score as Fast as Possible, Do This

I get asked this a lot, so here's my straight answer. If your credit score needs work and you want to move the needle as quickly as possible, these are the highest-impact actions in the order I'd prioritize them:

First, pull your credit reports and dispute any errors. This is the only move that can produce a meaningful score increase without changing your spending habits at all. If there's a late payment that was reported incorrectly, an account that isn't yours, or a collections entry that should have aged off, dispute it. The bureaus have 30 to 45 days to investigate, and if the error is removed, your score can jump in a single reporting cycle.

Second, pay down your credit card balances aggressively. If your utilization is above 30%, getting it below that threshold (and ideally below 10%) is the fastest behavioral change you can make. This one factor accounts for roughly 30% of your score, and the impact shows up as soon as your lower balance is reported, usually within a billing cycle. If you've got a tax refund, a bonus, or cash sitting in a low-interest savings account while you carry credit card debt, redirect it.

Third, set up autopay on everything. You cannot afford a single late payment while you're trying to build your score. Autopay the minimum on every account as a safety net, then manually pay more whenever you can. This eliminates the risk of a forgotten bill undoing months of progress.

Fourth, ask for credit limit increases on your existing cards. This lowers your utilization ratio instantly without requiring you to pay anything down. Call each issuer, ask for an increase, and make sure they can do a "soft pull" rather than a hard inquiry. Not every issuer will agree, but many will if you have a track record of on-time payments.

Fifth, become an authorized user on a family member's well-managed card. If someone close to you has a card with a long history, high limit, and perfect payment record, being added as an authorized user can import that positive history into your credit file. You don't even need to use the card. Just being on the account helps.

These five actions, done in this order, give you the best chance of seeing real improvement in 30 to 90 days. Beyond that, it's about consistency. There is no overnight fix for credit, but there is a 90-day fix, and it starts with knowing exactly where you stand.

Your credit score isn't a reflection of your worth as a person. But in the eyes of the financial system, it's the first thing anyone looks at. The good news? The rules are knowable, the game is winnable, and the best time to start playing it well is right now.