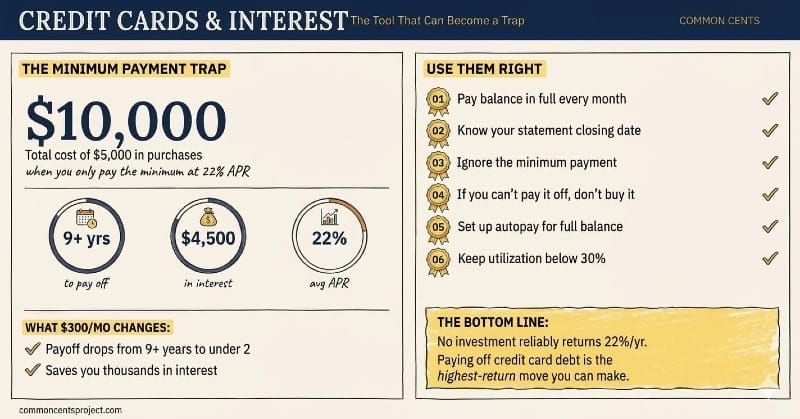

Credit Cards and Interest: The Tool That Can Become a Trap

The Bottom Line: A credit card is a short-term loan that renews every month. Pay it off in full and it costs you nothing. Carry a balance and you're paying 20 to 25% interest, making it one of the most expensive forms of borrowing in existence. The minimum payment is designed to keep you in debt, not help you get out of it.The math that matters: A $5,000 balance at 22% APR with minimum payments takes over 9 years to pay off and costs you nearly $10,000 totalThe one rule: If you can't pay it off this month, you can't afford to buy it this monthThe fastest win in personal finance: Paying off credit card debt. No investment reliably returns 22% per year, which is what you effectively earn by eliminating that balance

A credit card is a short-term loan that renews every month. You swipe, the bank pays the merchant, and you agree to pay the bank back. If you pay your full balance by the due date, you owe nothing extra. If you don't, the bank charges you interest on whatever you still owe. And that's where the trouble starts.

Credit card interest rates are brutal. The average APR hovers around 20 to 25%, making credit cards one of the most expensive forms of borrowing in existence. For context, a decent mortgage rate might be in the 6 to 7% range. Credit cards charge three to four times that.

The Minimum Payment Trap

Here's where the math gets painful.

Say you carry a $5,000 balance at 22% APR and make only the minimum payment, typically around $100. At that rate, it will take you over 9 years to pay off the balance, and you'll pay roughly $4,500 in interest alone. You'll have paid close to $10,000 for $5,000 worth of stuff. That's not a purchase. That's a trap.

The minimum payment is designed to keep you in debt. The bank makes money every single month you carry a balance. They are in no hurry for you to pay it off. Understanding this dynamic is one of the most important financial lessons you can learn.

Your credit card statement is actually required by law to show you how long it will take to pay off your balance if you only make minimums. Most people skip right past that box. Don't. Read it. Let the number sink in. That's your wake-up call.

How Credit Card Interest Actually Works

Most people think interest is charged once a month. It's not. Credit card interest is calculated daily. Your issuer takes your APR, divides it by 365 to get a daily rate, and applies that rate to your outstanding balance every single day. That daily charge gets added to your balance, which means tomorrow's interest is calculated on a slightly larger number. This is compounding working against you instead of for you.

Here's the other piece most people miss: the grace period. If you pay your full statement balance by the due date every month, you typically get 21 to 25 days of interest-free borrowing on new purchases. That grace period is the entire reason credit cards can be a great tool. But the moment you carry a balance from one month to the next, the grace period often disappears on new purchases too. You start accruing interest on everything immediately.

That means carrying a balance doesn't just cost you interest on the old debt. It can cost you interest on every new purchase from the moment you swipe.

What Credit Cards Cost You (Beyond Interest)

Interest is the biggest cost, but it's not the only one.

Late fees. Miss a payment and you'll typically get hit with a fee of $30 to $40. Miss two payments within six billing cycles and many issuers will bump you to a penalty APR, which can be as high as 29.99%. That penalty rate can apply to your entire balance, not just new purchases.

Annual fees. Some cards charge an annual fee in exchange for better rewards. This can make sense if you spend enough to earn back the fee in rewards and then some. But if you're carrying a balance and paying 22% interest, no amount of cash back or travel points is offsetting that cost. The rewards are a rounding error compared to the interest.

Cash advance fees. Using your credit card to withdraw cash from an ATM is one of the most expensive things you can do. Cash advances typically come with a fee of 3 to 5% of the amount withdrawn, a higher APR than purchases, and no grace period at all. Interest starts accruing immediately.

How to Use Credit Cards the Right Way

Credit cards aren't the enemy. Used correctly, they build your credit history, offer purchase protections, earn you real rewards, and give you a free short-term loan every single month. The key is treating them as a tool, not a source of money you don't have.

Pay your balance in full every month. This is the single most important rule. If you do this, a credit card is a free short-term loan with rewards attached. If you don't, those rewards get eaten alive by interest charges.

Know your statement closing date. Interest is typically calculated based on the balance reported when your statement closes, not your due date. If you make a large purchase, paying it off before the statement closes means a lower reported balance, which also helps your credit score.

Don't confuse the minimum payment with what you owe. The minimum is what the bank requires to keep your account in good standing. It is not a suggested payment amount. It's the amount designed to maximize how long you stay in debt.

Treat it like a debit card. If you can't pay it off this month, you can't afford to buy it this month. The moment you start carrying a balance, the cost of everything you bought just went up by 20% or more, compounding daily.

Set up autopay for the full balance. This eliminates the risk of a forgotten payment triggering a late fee or penalty APR. If you're worried about overdrafting your bank account, set autopay for the minimum as a safety net, but then manually pay the full balance before the due date.

Keep your utilization low. How much of your available credit you're using (your utilization ratio) is one of the biggest factors in your credit score. Aim to keep it below 30% of your limit, and below 10% if you want to optimize. If you have a $10,000 limit, try not to let your balance go above $1,000 when your statement closes.

If You're Already Carrying a Balance, Here's What to Do

If you're reading this and you already have credit card debt, don't panic. But do treat it as your number one financial priority.

Stop adding to the balance. This sounds obvious, but it's the hardest part. If you keep swiping while trying to pay down debt, you're filling the bathtub while trying to drain it.

Pay more than the minimum. As much more as you can. Every extra dollar you put toward your balance saves you interest and shortens your payoff timeline dramatically. Going from a $100 minimum to a $300 monthly payment on that $5,000 balance cuts your payoff time from 9 years to under 2 years and saves you thousands in interest.

Attack the highest interest rate first. If you have balances on multiple cards, make minimums on all of them but throw every extra dollar at the card with the highest APR. This is called the avalanche method, and it's the mathematically optimal approach.

Consider a balance transfer. Some cards offer 0% introductory APR on balance transfers for 12 to 21 months. If you can transfer your high-interest balance and pay it off within the promotional period, you'll save a significant amount in interest. Just watch for balance transfer fees (typically 3 to 5%) and make sure you have a realistic plan to pay it off before the promotional rate expires.

Call your card issuer and ask for a lower rate. It sounds too simple, but it works more often than you'd think. If you've been a reliable customer with on-time payments, many issuers will reduce your APR just because you asked. Even a few percentage points can save you hundreds of dollars.

No investment in the world reliably returns 22% per year. That means paying off credit card debt isn't just smart. It's the single highest-return financial move most people can make. If you're carrying a balance right now, making that your number one priority isn't optional. It's urgent.